1. What is the Filling Equipment Market Overview – definition, scope, and significance?

The Filling Equipment Market encompasses all machinery and systems used to dispense products into containers across various industries. It includes equipment classified by process type (manual, semi‑automatic, automatic), by product form (solid, semi‑solid, liquid, powder), and by end‑user sectors such as food & beverage, pharmaceutical, and cosmetic. The market’s significance lies in its role as a critical enabler of efficient, hygienic, and high‑speed packaging operations, directly influencing product quality, safety, and cost competitiveness for manufacturers worldwide.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Filling Equipment Market?

Key drivers include rising demand for packaged goods, stringent hygiene regulations, and the push for automation to reduce labor costs. Restraints stem from high capital investment requirements and the complexity of integrating new technologies with legacy lines. Challenges involve maintaining equipment uptime in fast‑changing production environments and meeting diverse packaging formats. Opportunities arise from emerging smart‑filling solutions, sustainability trends encouraging reduced waste, and the growth of specialty segments such as high‑value cosmetics and personalized pharmaceuticals.

3. Which growth trends are currently influencing the Filling Equipment Market?

Current trends feature the adoption of Industry 4.0 connectivity, allowing real‑time monitoring and predictive maintenance. There is a clear shift toward fully automatic lines to achieve higher throughput and lower labor dependence. Multi‑product flexibility is gaining traction, enabling manufacturers to switch between liquids, powders, and semi‑solids on a single line. Additionally, the rise of e‑commerce and smaller pack formats is driving demand for compact, high‑precision filling solutions.

4. How did COVID‑19 impact the Filling Equipment Market, and what is the recovery trajectory?

The pandemic caused short‑term disruptions in supply chains and delayed capital projects, especially in the early 2020‑2021 period. However, heightened consumer demand for packaged food, beverages, and health‑related products accelerated equipment orders in the latter half of 2021. Recovery has been robust, with manufacturers accelerating automation to mitigate future disruptions, positioning the market on a steady growth path.

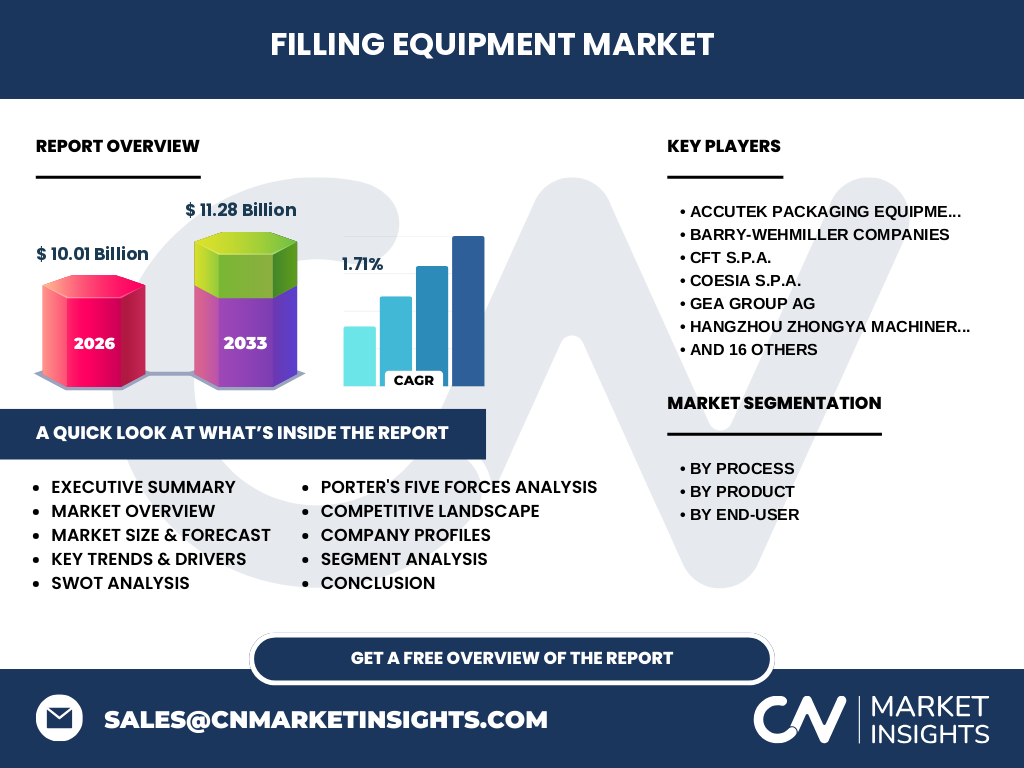

5. Who are the major competitors in the Filling Equipment Market and what is the level of market consolidation?

Key competitors include Accutek Packaging Equipment Company, Inc., Barry‑Wehmiller Companies, CFT S.p.A., COESIA S.p.A., GEA Group AG, Hangzhou Zhongya Machinery Co., I.M.A. Industria Macchine Automatiche S.p.A., JBT Corporation, KHS GmbH, Krones AG, Optima Packaging Group GmbH, Pro Mach, Inc., Ronchi Mario S.p.A., Scholle IPN, Serac Group, Shibuya Corporation, Sidel Group (Tetra Laval), Simik Inc., Swiss Can Machinery AG, Syntegon Technology GmbH (Bosch Packaging Technology), and Tetra Laval International S.A. The market shows moderate consolidation, with several large multinational firms owning extensive product portfolios, while niche specialists maintain strong positions in specific process or product segments.

6. What are the high‑level findings highlighted in the Executive Summary?

The Filling Equipment Market is valued at USD 10.01 billion in 2026 and is projected to reach USD 11.28 billion by 2033, reflecting a CAGR of 1.71 % over the forecast horizon. Growth is driven by automation, regulatory compliance, and expanding end‑user sectors. Manual and semi‑automatic segments remain important for low‑volume applications, whereas automatic systems dominate high‑speed, high‑volume lines. Geographic expansion, especially in emerging economies, presents significant upside, while digitalization offers a pathway to higher efficiency and lower total cost of ownership.

7. What is the market forecast for the Filling Equipment Market from 2025 to 2032?

Based on the provided CAGR of 1.71 %, the market is expected to sustain modest but steady growth through 2032. By 2032, the market size is anticipated to exceed USD 12 billion, driven by continued automation adoption, product diversification, and increasing demand from food & beverage, pharmaceutical, and cosmetic manufacturers seeking more precise and hygienic filling solutions.

8. How is the Filling Equipment Market sized and shared by segmentation?

By Process: Manual equipment serves low‑volume, niche applications; semi‑automatic solutions bridge the gap for medium‑scale producers; automatic systems dominate large‑scale operations requiring high throughput. By Product: Liquid filling holds the largest share due to the expansive beverage and pharma markets, followed by powder and semi‑solid segments that cater to food additives and cosmetics. By End‑user: Food & beverage leads the market, reflecting the volume of packaged consumables, while pharmaceutical and cosmetic sectors are growing rapidly as they require higher precision and compliance.

9. What is the global geographic distribution of the Filling Equipment Market?

The market is globally distributed, with strong presence in North America and Europe where automation levels are high. Asia‑Pacific shows the fastest growth, fueled by expanding food & beverage production and increasing pharmaceutical manufacturing capacity. Latin America and the Middle East present emerging opportunities as local companies upgrade legacy lines.

10. What are the detailed regional performances within the Filling Equipment Market?

North America remains a mature market with high adoption of automatic filling lines, driven by stringent food safety standards. Europe mirrors this trend, with added emphasis on sustainability and energy‑efficient equipment. In Asia‑Pacific, China, India, and Southeast Asian nations are investing heavily in modernizing packaging lines, creating demand for both semi‑automatic and automatic solutions. The Middle East and Africa exhibit incremental growth as multinational equipment suppliers establish regional service hubs.

11. Which companies lead the Filling Equipment Market and what are their strategic approaches?

Leaders such as Krones AG, Tetra Laval, and GEA Group AG focus on integrated turnkey solutions, combining filling technology with downstream packaging. JBT Corporation and Syntegon Technology emphasize modular, scalable systems that can be upgraded as production needs evolve. Regional players like Hangzhou Zhongya Machinery and CFT S.p.A. target cost‑sensitive markets with competitively priced semi‑automatic equipment. Partnerships, joint ventures, and acquisitions are common tactics to broaden product portfolios and geographic reach.

12. How does Porter’s Five Forces model apply to the Filling Equipment Market?

• Threat of new entrants: Moderate – high capital costs and technical expertise create barriers, yet niche innovators can enter with specialized solutions. • Bargaining power of suppliers: Low to moderate – component suppliers are abundant, but high‑precision parts can give select vendors leverage. • Bargaining power of buyers: Moderate – large manufacturers can negotiate price and service terms, while smaller users have limited leverage. • Threat of substitutes: Low – alternative packaging methods (e.g., spray‑drying) do not replace the core function of precise filling. • Competitive rivalry: High – many global and regional firms compete on technology, price, and service quality.

13. What are the primary strengths, weaknesses, opportunities, and threats for the Filling Equipment Market?

Strengths include essential role in product packaging, ongoing demand across diverse industries, and strong innovation pipelines. Weaknesses involve the capital‑intensive nature of equipment and the need for skilled technicians. Opportunities arise from digital integration, sustainable design, and expanding into emerging markets. Threats consist of economic downturns that delay capital spending and potential regulatory changes that increase compliance costs.

14. How is the value chain structured in the Filling Equipment Market?

The value chain starts with raw material suppliers (metals, electronics, hydraulic components), moves to equipment designers and manufacturers, followed by system integrators who customize lines for specific clients. After‑sales service, spare‑parts logistics, and end‑user training form the downstream segment, creating recurring revenue streams and reinforcing customer loyalty.

15. What investment insights are essential for stakeholders in the Filling Equipment Market?

Investors should prioritize companies with strong R&D pipelines focused on Industry 4.0 capabilities, as these solutions command premium pricing and recurring service contracts. Geographic diversification, especially into Asia‑Pacific, offers higher growth potential. Partnerships with OEMs in high‑value end‑user sectors (pharma, cosmetics) can secure long‑term contracts, enhancing revenue stability.

16. What are the key takeaways from the Filling Equipment Market analysis?

The market is poised for steady growth, underpinned by automation, regulatory pressure, and expanding consumer demand for packaged goods. While the CAGR of 1.71 % suggests moderate expansion, the shift toward smart, sustainable filling solutions creates differentiated value for manufacturers. Companies that blend technology leadership with global service networks are likely to capture the most market share.

17. How was the research methodology designed for this report?

The study employed a mixed‑method approach combining secondary data collection from industry publications, company annual reports, and reputable market databases with primary interviews of senior executives from leading equipment manufacturers and end‑user firms. Quantitative data were triangulated to validate the market size of USD 10.01 billion (2026) and the projected USD 11.28 billion (2033). Trend analysis leveraged both macro‑economic indicators and technology adoption metrics.

18. What is the scope of this research and its limitations?

The scope covers global filling equipment used for solids, semi‑solids, liquids, and powders across food & beverage, pharmaceutical, and cosmetic end‑users. It excludes niche niche equipment for non‑packaging applications (e.g., bulk material handling). While the analysis draws on the latest available data, rapid technological shifts or sudden regulatory changes could affect future forecasts.

19. Which key companies have made notable recent developments in the Filling Equipment Market?

Recent announcements include Krones AG’s launch of an AI‑driven liquid filling platform, Tetra Laval’s partnership with a leading pharmaceutical firm for sterile powder filling lines, and Syntegon Technology’s rollout of a modular automatic system for cosmetic jars. GEA Group introduced a new energy‑efficient semi‑automatic filler targeting small‑batch food producers, while JBT Corporation acquired a digital sensor specialist to enhance predictive maintenance capabilities.